Advertisement

Advertisement

Week Ahead: Tariffs and US Jobs Data in the Spotlight

By:

The FP Markets Week-Ahead release highlights key macro drivers to be aware of for the upcoming trading week.

Where We Were

Despite the holiday-shortened week, the tariff dial was firmly turned up a notch.

The beginning of the week kicked off with US President Donald Trump recommending a 50% levy on the European Union (EU), effective 1 June, claiming that the EU ‘has ‘been very difficult to deal with’. However, following a call with European Commission President Ursula von der Leyen, Trump agreed to extend the deadline to 9 July.

Mid-week, however, the majority of Trump’s global tariffs were legally reined in, understandably triggering a risk-on bid across the markets. The US Court of Trade ruled against most of the tariffs, determining that they were illegal under the International Emergency Economic Powers Act (IEEPA). Then on Thursday, Trump received a temporary reprieve from a Federal Appeals court, meaning, for now at least, all tariffs remain in effect, with Trump’s team appealing the initial ruling.

As you would expect, Trump was also vocal in response to recent events, commenting via his Truth Social platform that the ruling ‘is so wrong, and so political!’ While the Trump administration celebrated this temporary victory, it also indicated that other legal avenues exist for imposing tariffs if appeals fail. However, these alternatives are generally more time-consuming and could limit the range of future tariff actions.

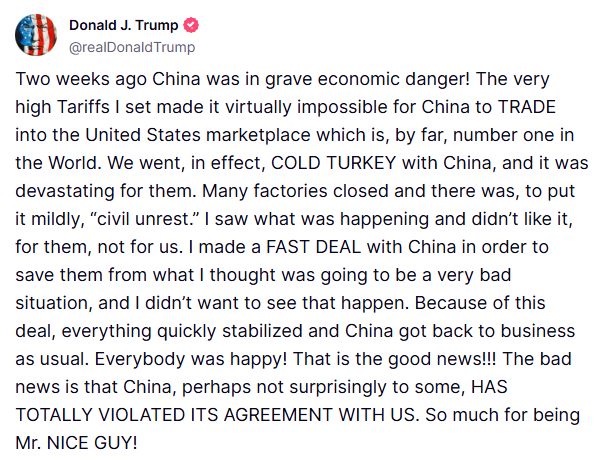

It did not end there. Adding to the week’s trade tensions, Trump also targeted China on Friday. In a social media post, he noted that he made a ‘FAST DEAL’ with China, and that they have ‘VIOLATED ITS AGREEMENT’. As you can see from the screenshot below, Trump did not provide specifics about what the agreement entailed.

Although we are now two months in following Trump’s ‘Liberation Day’, and unless I have missed something, ‘uncertainty’ remains the prevailing sentiment across markets and businesses.

Where We Are

In addition to trade developments remaining front and centre for market participants this week, the upcoming data slate has a lot going on. This includes updates from the European Central Bank (ECB) and the Bank of Canada (BoC), as well as a focus on US jobs data.

ECB to Cut Rates by 25 Basis Points

Markets are fully pricing in that the ECB will reduce its benchmark rates by another 25 basis points (bps) on Thursday, bringing the deposit facility rate to 2.00% and the refinancing rate to 2.15%. A reduction this week would mark the eighth rate cut since the central bank initiated its easing cycle in mid-2024. According to market pricing, it could also represent the penultimate rate cut, with a final 25 bp reduction anticipated at the end of the year.

This comes alongside several desks expecting GDP (Gross Domestic Product) growth to take a hit in Q2 25, as well as CPI inflation data (Consumer Price Index) for the eurozone remaining stable at 2.2% in April year-on-year (YY) and economists expecting May’s inflation reading to reach the central bank’s inflation target of 2.0% (released this week). Bolstering Europe’s disinflationary picture, regional inflation recently showed cooling price pressures; inflation in Germany remained at 2.1% in May YY, and cooled to 0.7% in France for May YY, down from 0.8% in April.

While a rate cut is likely a done deal, it is no secret that divisions exist among the ECB Governing Council members; therefore, it is unrealistic to expect the decision to be unanimous. For example, ECB’s Šimkus and Rehn support further rate cuts, while ECB’s Holzmann advocates maintaining current rates.

Given the above, I believe the majority of attention at this week’s meeting will be focused on the ECB’s language (trade developments, in particular) and the macroeconomic projections. It is likely that the ECB will revise its headline inflation forecast lower – with many desks attributing this to a stronger euro (EUR) and softer energy prices – as well as GDP growth being revised slightly downward. Like the US Federal Reserve (Fed), I also expect a similar wait-and-see stance to be emphasised by the ECB, meaning the forward guidance could be vague given US trade policy.

Were the ECB to hint that the end of the easing cycle is near, aligning with market pricing, this would likely support a bid in EUR/USD (euro versus the US dollar), particularly given that the Fed has more work to do on policy easing.

EUR Bulls Expected to Remain On the Offensive

Technically, I remain EUR bullish versus the USD in the medium term. As shown on the charts below, price action on the monthly timeframe witnessed resistance at US$1.1457 enter the fray. This triggered a subsequent retest of support from US$1.1134, which, as you can see, held firm in May. Given this, US$1.1457 is perhaps vulnerable to the upside, targeting resistance between US$1.2028 and US$1.1930.

Supporting this bullish outlook, and understanding the story on the monthly chart, I believe there is limited downside potential left from the ‘alternate’ AB=CD resistance level on the daily chart from US$1.1386 (a 1.272% Fibonacci projection ratio) – a base complemented by a 61.8% Fibonacci retracement ratio from US$1.1383. You can see price has connected with US$1.1283 – the 38.2% Fibonacci retracement ratio derived from legs A-D (US$1.1065-US$1.1419), which is a common AB=CD profit objective, and came within striking distance of US$1.1200, another widely followed profit objective (61.8% Fibonacci retracement ratio) before rebounding to the upside. This could potentially unearth a long opportunity on the break of US$1.1386, targeting US$1.1573, a year-to-date high formed in April.

Markets Expect BoC to Hold Ground

The BoC is forecast to remain on hold at 2.75% on Wednesday.

With Canada’s core CPI inflation measures remaining elevated – both CPI Trim and Median rose strongly in April, manoeuvring above the BoC’s 1% – 3% inflation target band – and Q1 25 GDP matching the pace of Q4 24, growing by 0.5%, the odds of a hold decision has been largely priced in. Market pricing implies a 75% chance that the central bank keeps the rate unchanged, versus a 25% probability of another 25-bp cut, which would bring the overnight rate to 2.50%.

A hold decision, therefore, could increase demand for the Canadian dollar (CAD), weighing on the USD/CAD. Notably, although the usual rate statement and press conference will take place, it is worth noting that no updated macroeconomic forecasts will be released at this meeting.

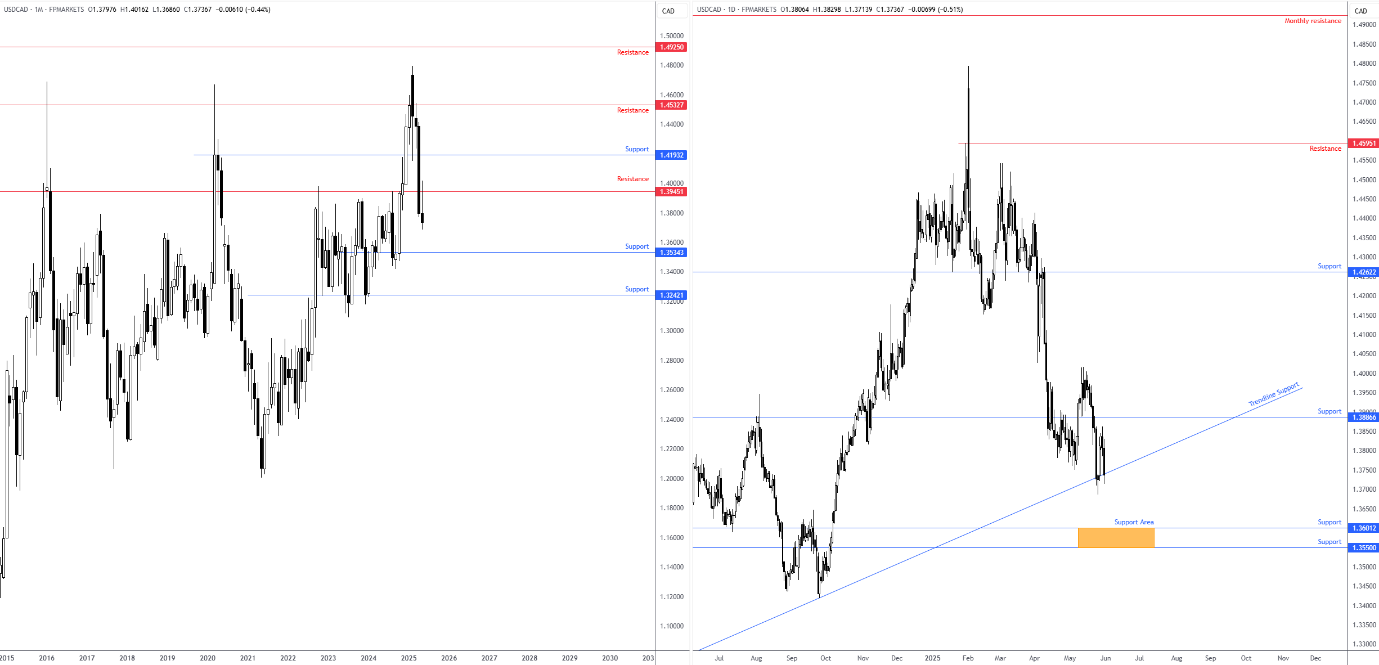

USD/CAD Downhill from Here?

C$1.3945 was made short work of in April and retested as resistance in May, following a fourth consecutive month in the red. Technically speaking, the scope to explore deeper water is evident on the monthly scale until C$1.3534, followed by another layer of support from C$1.3242.

In view of this, as well as the lack of bullish intent evident from trendline support on the daily chart last week, extended from the low of C$1.2007, a breakout lower here could trigger further downside towards a daily support area between C$1.3550 and C$1.3601.

US Jobs Data in View

Amid a slowdown in soft US data, investors will closely monitor the US employment situation report for May for signs of cooling, which is released on Friday. As of writing, analysts are expecting the US economy to have added 130,000 new payrolls, marking a slowdown from April’s stronger-than-expected reading of 177,000. The unemployment rate is anticipated to remain at 4.2%, while wages are forecast to have risen by 0.3% month-on-month (from 0.2%) and to have ticked lower to 3.7% YY (from 3.8%).

If unemployment remains steady and wages rise, this reinforces a robust labour market and could be positive for the USD. However, should data come in weaker-than-expected, a USD selloff might be in the offing, as this could increase the odds of the Fed cutting rates at July’s meeting (currently 7 bps of easing priced in).

You may recall from the minutes of the Fed meeting that the central bank emphasised its ‘wait-and-see’ stance, and underscored that they remain ‘well-positioned to wait for more clarity on the outlook for inflation and economic activity’.

Additionally, as I noted in a post last week, Fed officials underscored that downside risks to employment and economic activity, as well as upside risks to inflation, have increased, primarily due to Trump’s tariff increases. I’ve also noted several times that this places the Fed in a challenging spot: they can either keep interest rates high to fight potential inflation or lower them to boost the economy. Markets expect the Fed to hold rates at its upcoming meeting this month, with investors looking to the September meeting for a 25 bp rate cut and a total of 50 bps of easing priced in for the year.

Ahead of Friday’s jobs report, several employment metrics are also making the airwaves this week. On Tuesday, April’s job openings figures land, shedding light on labour demand. Wednesday brings the ADP (Automatic Data Processing) private payrolls report for May, providing insights into private sector employment trends. Then, on Thursday, the latest weekly jobless claims will indicate movements in unemployment insurance applications – the latest print saw initial claims rise by 240,000 and continuing claims increase by 1.919 million, both of which were higher than expected.

We’ll also gain insight into how tariff uncertainty has affected business activity and confidence with the release of the latest ISM data (Institute for Supply Management) for May. The ISM Manufacturing PMI (Purchasing Managers’ Index) will be released on Monday, providing an update on the latest developments in the manufacturing sector. This will be followed by the ISM Services PMI on Wednesday, which will offer a read on the much larger services sector.

Charts created using TradingView

Written by FP Markets Chief Market Analyst Aaron Hill

DISCLAIMER:

The information contained in this material is intended for general advice only. It does not take into account your investment objectives, financial situation or particular needs. FP Markets has made every effort to ensure the accuracy of the information as at the date of publication. FP Markets does not give any warranty or representation as to the material. Examples included in this material are for illustrative purposes only. To the extent permitted by law, FP Markets and its employees shall not be liable for any loss or damage arising in any way (including by way of negligence) from or in connection with any information provided in or omitted from this material. Features of the FP Markets products including applicable fees and charges are outlined in the Product Disclosure Statements available from FP Markets website, www.fpmarkets.com and should be considered before deciding to deal in those products. Derivatives can be risky; losses can exceed your initial payment. FP Markets recommends that you seek independent advice. First Prudential Markets Pty Ltd trading as FP Markets ABN 16112 600 281, Australian Financial Services License Number 286354.

About the Author

Aaron Hillcontributor

Aaron graduated from the Open University and pursued a career in teaching, though soon discovered a passion for trading, personal finance and writing.

Advertisement