Advertisement

Advertisement

First Light News: USD Lower On Dovish Fed Chair Successor

By:

In addition to more Fed speak today, we also have Bank of England Governor Andrew Bailey scheduled to deliver a speech at the British Chambers of Commerce in London.

The US dollar (USD) chalked up another leg lower yesterday – boosting the euro [EUR] and British pound [GBP]) – partly aided by reports that US President Donald Trump will announce the successor to US Federal Reserve (Fed) Chairman Jerome Powell sooner than expected. According to the Wall Street Journal, this could be announced as soon as September, with names in the frame including US Treasury Secretary Scott Bessent, former Fed Governor Kevin Warsh, as well as Fed Governor Christopher Waller. I think it is clear that Trump will choose a Chair who supports his policy goals, leading markets to interpret the news as dovish.

While Trump has repeatedly called for lower rates, along with a few Fed officials – including Fed Governors Michelle Bowman and Christopher Waller – advocating for a July rate cut, Powell maintains that the economy remains in good shape and continues to adopt a ‘wait-and-see’ stance amid global economic uncertainty. This was emphasised at Powell’s two-day testimony before Congress this week.

Despite the USD exploring lower levels in response to the news, rate pricing is largely unchanged: 63 basis points (bps) worth of cuts are priced in for the year, with September’s meeting fully discounted for the first 25 bp reduction.

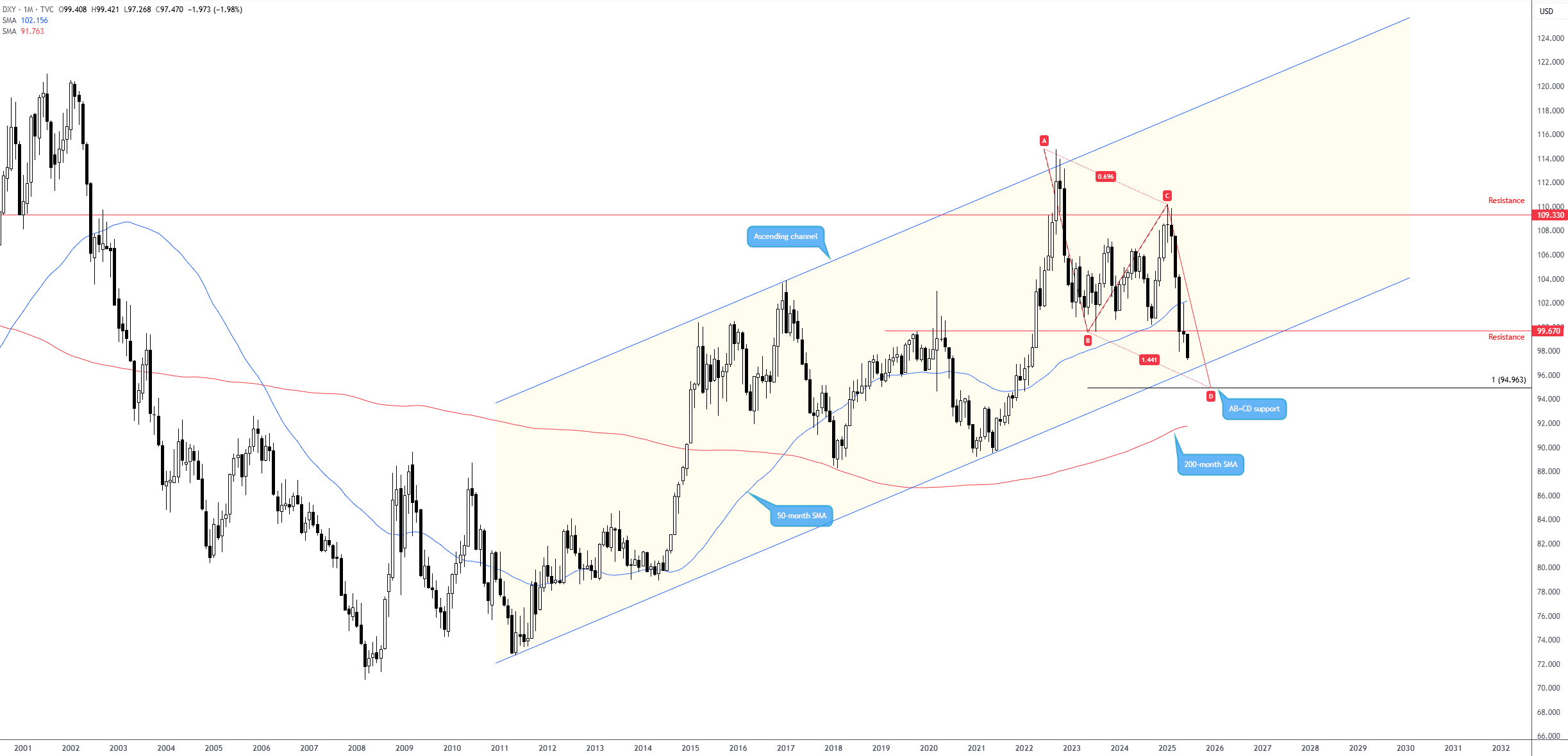

As shown below, the USD Index manoeuvred through a punchy monthly support at 99.67 in May (now a marked resistance), suggesting a continued bearish narrative until monthly channel support, pencilled in from the low of 72.70. It may also be worth acknowledging that breaching this channel support could open the door to further underperformance towards a 100% projection ratio of 94.96, forming a clear-cut monthly AB=CD equal support formation.

Other News

- At the NATO summit (North Atlantic Treaty Organisation) in the Hague, Trump has committed to Article 5 amid a boost in defence spending of 5% of member GDP (Gross Domestic Product) by 2035. Although this deal is an important victory for Trump and NATO Secretary General Mark Rutte, some members, such as Slovakia and Spain, have voiced concerns about their capacity to reach the higher spending targets.

- The Big Beautiful Bill’s deadline of 4 July is fast approaching. Trump is intensely pushing the Senate to pass the Bill by the deadline, urging them to stay until the job is done. Via his Truth Social platform, the President voiced the following: ‘To my friends in the Senate, lock yourself in a room if you must, don’t go home, and GET THE DEAL DONE THIS WEEK. Work with the House so they can pick it up, and pass it, IMMEDIATELY. NO ONE GOES ON VACATION UNTIL IT’S DONE’.

- In the equity space, Nvidia (NVDA) clawed back recent losses. It climbed to record highs yesterday, overtaking Microsoft (MSFT) to reclaim the title of the world’s most valuable company in terms of market capitalisation (US$3.77 trillion). The NVDA stock rose by 4.3% following the optimistic outlook from Nvidia’s CEO, Jensen Huang, at the company’s annual shareholder meeting. Huang highlighted the ‘multitrillion-dollar opportunity’ in AI (Artificial Intelligence) and robotics, signalling a decade-long AI infrastructure build-out.

Day Ahead

In addition to more Fed speak today, we also have Bank of England Governor Andrew Bailey scheduled to deliver a speech at the British Chambers of Commerce in London at 11:00 am GMT, and European Central Bank Christine Lagarde is due to give an opening speech at the Munich Opera Festival at 6:30 pm GMT.

On the data front, the focus will be stateside, with the majority of data expected to land at 12:30 pm GMT. This includes the final estimate for Q1 25 GDP, expected to show a 0.2% decline, weekly jobless filings for the week ending 21 June, May durable goods orders, and May pending home sales (2:00 pm GMT).

Charts created using TradingView

Written by FP Markets Chief Market Analyst Aaron Hill

About the Author

Aaron Hillcontributor

Aaron graduated from the Open University and pursued a career in teaching, though soon discovered a passion for trading, personal finance and writing.

Advertisement